No matter the size or type of your company, managing cash flow is essential, and often difficult. Many businesses need help in the form of financing to smooth out their cash flow cycles.

Debt factoring is an increasingly popular form of funding for Australian businesses. It basically involves ‘selling’ your accounts receivables in exchange for fast access to cash.

But how does debt factoring work? And how can it improve your cash flow? Read on to find out more.

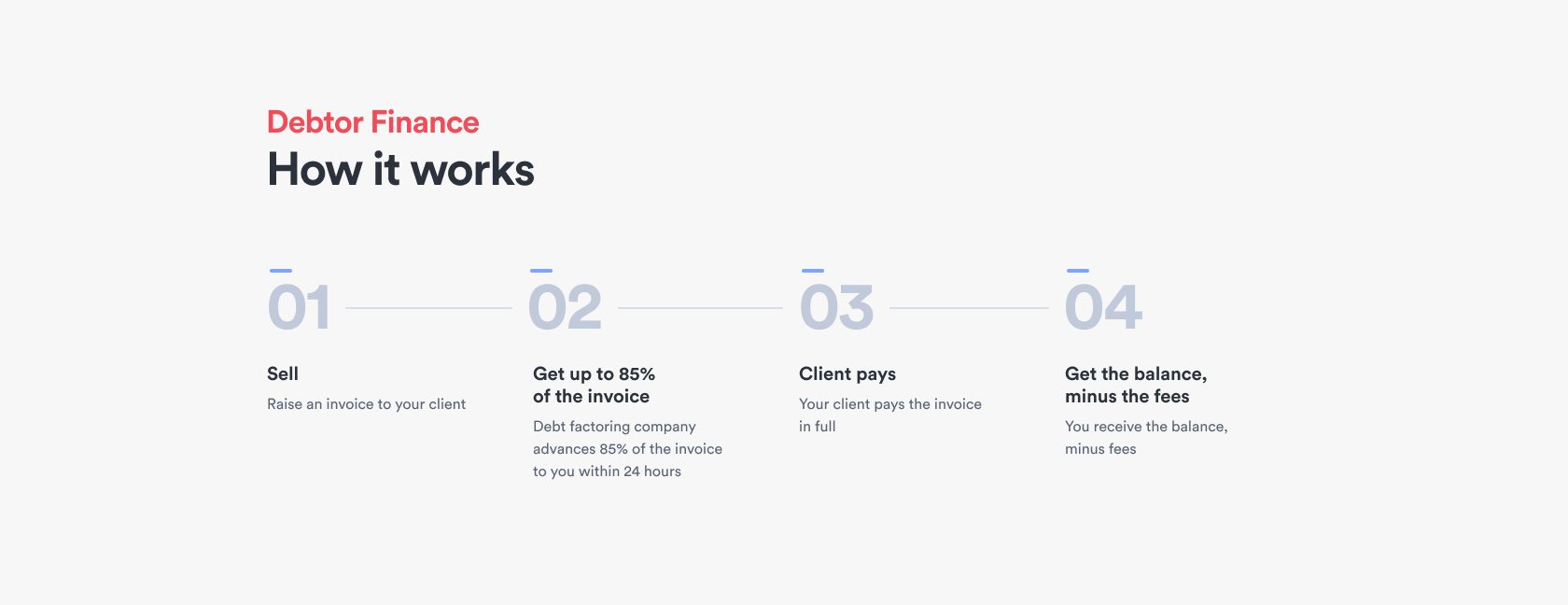

How does debt factoring work?

Debt factoring is a way to fund your business by using the largest asset your business has – your accounts receivable.

It works by ‘selling’ your outstanding customer invoices (accounts receivable) to a debt factoring company. The company, known as a financier, ‘buys’ those invoices for up to 85% of their value which you can then use immediately in your business, rather than waiting for your customer to pay. Your financier then collects the full invoice payment from your client and pays you the outstanding amount, minus whatever they charge as their fee.

Why debt factoring is so powerful

It’s not hard to see how debt factoring can help your business with cash flow.

After all, imagine if your customers paid you within 24 hours of receiving their invoices.

Think about what you could do with your business:

- Where could you take it?

- How many more opportunities for growth could you take advantage of?

- What financial benefits could you take advantage of by paying your suppliers faster?

Having your funds in your bank account within a day gives you essential working capital. You can use it to pay expenses – or as base capital to fund business expansion. Imagine the possibilities!

Of course, in the real world, your customers just aren’t going to pay you within 24 hours. They’re all managing their own cash flow, so it’s almost never in their best interests to pay your invoices early. But that net effect – up to 85% of your invoices paid up front – is essentially what debt factoring provides.

In essence, debt factoring opens up more finance, more quickly, than you can achieve by any other business funding means.

How does debt factoring improve cash flow?

Debt factoring improves cash flow by giving your business significantly faster access to revenue owed to you.

It means you never have to wait the full term of your invoice to get your cash. And that’s important, because waiting 30, 60 or 90 days to be paid can put a severe strain on your business. In fact, of the 8,000+ companies that declared insolvency in 2018/19, more than half – 51% – reported inadequate cash flow as the reason.

That’s not surprising, given the average time taken to pay invoices by Australian businesses is 33 days. Sadly, the average time it takes big businesses to pay small businesses is even worse. So consider how powerful it would be to get your money almost immediately via debt factoring. Then it’s there and available for you to:

- pay your bills and business expenses (e.g. wages, rentals, tax and insurances)

- buy supplies or equipment

- grow your business… without that extended wait.

Without instant access to the money locked up in your accounts receivable, however, you need to fund all of the above from your profits or working capital. That means that – unless your cash flow is particularly strong from other sources – your business can’t grow. You can’t take on new work and opportunities if you don’t have the cash flow to support them.

It’s also important to realise that cash flow isn’t something you can sort out once and never think about again. Running a successful business means maintaining a strong, steady cash flow over time. Luckily, debt factoring isn’t just a one-off loan. It gives you ongoing access to cash flow, like a line of credit. As you raise more invoices, you have access to more cash.

Let’s say you made $500,000 worth of sales in January. Debt factoring would give you up to $425,000 of that almost immediately. If you then took on new contracts, won new customers and increased your sales to $600,000 in February, your available amount would rise to up to $510,000, depending upon the agreed facility size.

This more immediate cash flow benefit can help to accelerate your business growth, which in turn could lead to more available cash flow.

Other advantages of debt factoring

Improved cash flow isn’t the only advantage of debt factoring. It also provides:

- A flexible alternative to traditional financing. Traditional funding methods like loans and overdrafts generally require some form of security – usually property or other assets. That may not always be an option, especially if you don’t own property or have little equity to leverage. Alternative finance options like debt factoring don’t require directors’ personal assets as security. Your business simply funds itself and grows in line with its receivables.

- Freedom from stress. Don’t underestimate the positive impact on your mental health of no longer having to stress about cash flow. An MYOB survey found an unacceptable 52% of business owners have experienced increased stress and anxiety due to late payments and the cash flow issues they cause. Debt factoring can allow you to focus on planning your business, rather than fighting cash flow fires.

How much does factoring your accounts receivable cost?

You may be thinking that all this ‘factoring your accounts receivable’ sounds great… but how much will it cost?

There’s a perception that it’s expensive, but the reality is that the cost is on par with bank finance (without the personal security constraints) – and far less than any credit cards you use to smooth out your cash flow.

The actual fees vary, depending on several factors like:

- your sales volume

- the industry you’re in

- how stable your business is

- what payment terms you use

- how creditworthy your customers are

We can help you to understand the fees if you’d like to discuss your options.

How can Octet help my business’s cash flow?

At Octet, we have a range of flexible financing solutions to suit different businesses, including Debtor Finance, Trade Finance and Supply Chain Accelerate.

All of these financing solutions can be used as your primary funding source or to supplement other funding sources like bank loans. And since they aren’t generally classed as ‘debt’ from an accounting standpoint, they don’t affect your ability to access more traditional funding methods.

Our most flexible option for businesses that are growing fast is Debtor Finance.

Do you have a growing business, with great ambition and potential? Have you been trading for at least 6 months to 1 year, with a minimum AUD 1 million turnover? (That said, we can also look at start-ups, depending on your history). If so, you might be eligible for Debtor Finance.

Like many growing businesses, you may be facing cash flow challenges or looking to recapitalise so you can free up your cash flow. You may want to inject that cash into your business to make more sales, and – in turn – generate more profits. Does that sound like you?

Then, Octet’s Debtor Finance facility could be your answer. It gives you access to funding that increases as your business grows, so you can accelerate your growth and take advantage of new opportunities.

We’ve seen clients grow over just a few years from having a $100,000 Debtor Finance facility to $4 million, powered by the more flexible cash flow our Debtor Finance solution gives them.

Unlock the power of your receivables and improve your cash flow

Find out more about Debtor Finance today.

The comments and views in this communication are those of the author as at the date of this post and are subject to change without notice. This communication should not be construed as advice and you should act using your own information and judgment. Whilst information has been obtained from and is based upon multiple sources the author believes to be reliable, we do not guarantee its accuracy and it may be incomplete or condensed.